》View SMM Copper Prices, Data, and Market Analysis

》Subscribe to Access SMM Historical Spot Metal Prices

The topic of production cuts at Chinese copper smelters has remained a hot issue. Since the end of 2023, some small and medium-sized smelters have implemented disguised production cuts by reducing the efficiency of copper concentrate feeding, shutting down production lines, lowering the grade of copper concentrate fed into furnaces, and increasing the proportion of copper-containing materials in the feed.

With spot TC for copper concentrates repeatedly hitting new lows and China's smelting capacity for blister copper continuing to expand, the topic of smelter production cuts has been reignited. Currently, the SHFE futures market structure has shifted from a fully Contango structure to a near-month (SHFE copper 2503–SHFE copper 2605) Contango and far-month (SHFE copper 2506–SHFE copper 2602) Backwardation structure. The market is focusing on whether there will be unexpected production cuts in smelters' copper cathode production and whether such cuts will occur earlier or accelerate the shift of the Backwardation structure to the near month.

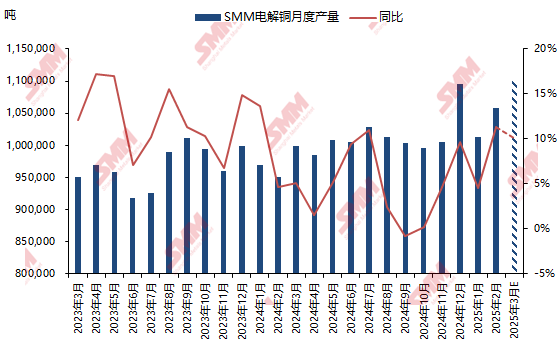

However, based on statistical data, monthly copper cathode production nationwide has not decreased but has instead continued to rise, exceeding 1 million mt per month. In February, SMM's China copper cathode production reached 1.0582 million mt, up 44,400 mt MoM (4.38%) and up 11.35% YoY, exceeding the expected 1.0554 million mt by 2,800 mt. March domestic copper cathode production is expected to reach 1.1002 million mt, up 42,000 mt MoM (3.97%) and up 100,700 mt YoY (10.08%). Cumulative production from January to March is expected to total 3.1722 million mt, up 252,600 mt YoY (8.65%).

In fact, the market's expectation of smelter production cuts refers to a significant reduction in China's monthly copper cathode production. While there may be some fluctuations between monthly production levels, the likelihood of such a scenario occurring is relatively small.

1. Despite facing a challenging market environment and high raw material prices, smelters with state-owned and central state-owned enterprise backgrounds, which account for the majority of capacity, prioritize social responsibility and local economic development over economic benefits. Therefore, these smelters are unlikely to voluntarily cut production.

2. Smelters with private enterprise backgrounds must maintain a certain operating rate to prevent banks from withdrawing loans and to avoid cash flow disruptions. If the main business of private smelters declines, it could trigger widespread loan withdrawals or short-term loan reductions by banks. Hence, private smelters are also motivated to sustain production.

3. Even if some state-owned or central state-owned smelters experience passive production cuts, the raw material shares released by these individual smelters will be absorbed by other smelters. This is another reason why China's monthly copper cathode production continues to "climb steadily."

》Click to View the SMM Copper Industry Chain Database